R语言学习笔记(十三):时间序列

Posted Ghost House

tags:

篇首语:本文由小常识网(cha138.com)小编为大家整理,主要介绍了R语言学习笔记(十三):时间序列相关的知识,希望对你有一定的参考价值。

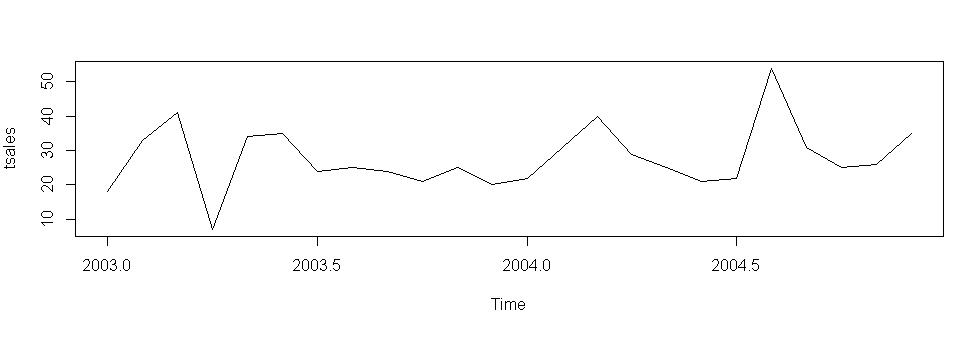

#生成时间序列对象 sales<-c(18,33,41,7,34,35,24,25,24,21,25,20,22,31,40,29,25,21,22,54,31,25,26,35) tsales<-ts(sales,start=c(2003,1),frequency = 12) tsales

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2003 18 33 41 7 34 35 24 25 24 21 25 20

2004 22 31 40 29 25 21 22 54 31 25 26 35

plot(tsales)

start(tsales) [1] 2003 1

end(tsales)

[1] 2004 12

frequency(tsales)

[1] 12

tsales.subset<-window(tsales,start=c(2003,5),end=c(2004,6)) tsales.subset

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2003 34 35 24 25 24 21 25 20

2004 22 31 40 29 25 21

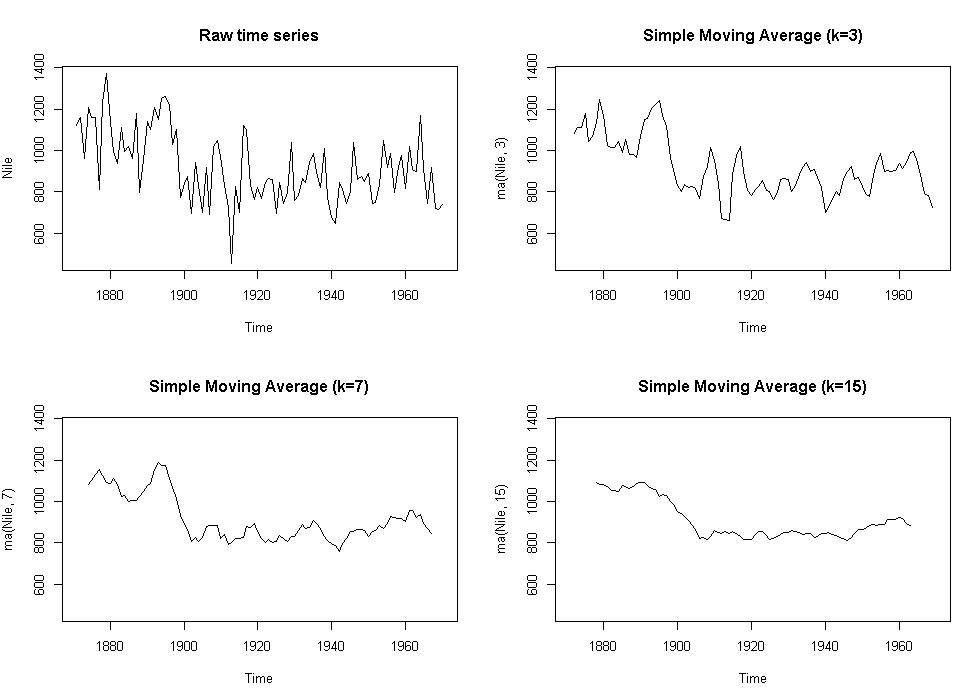

#简单移动平均

install.packages("forecast")

library(forecast)

opar<-par(no.readonly=TRUE)

par(mfrow=c(2,2))

ylim<-c(min(Nile),max(Nile))

plot(Nile,main="Raw time series")

plot(ma(Nile,3),main="Simple Moving Average (k=3)",ylim=ylim)

plot(ma(Nile,7),main="Simple Moving Average (k=7)",ylim=ylim)

plot(ma(Nile,15),main="Simple Moving Average (k=15)",ylim=ylim)

par(opar)

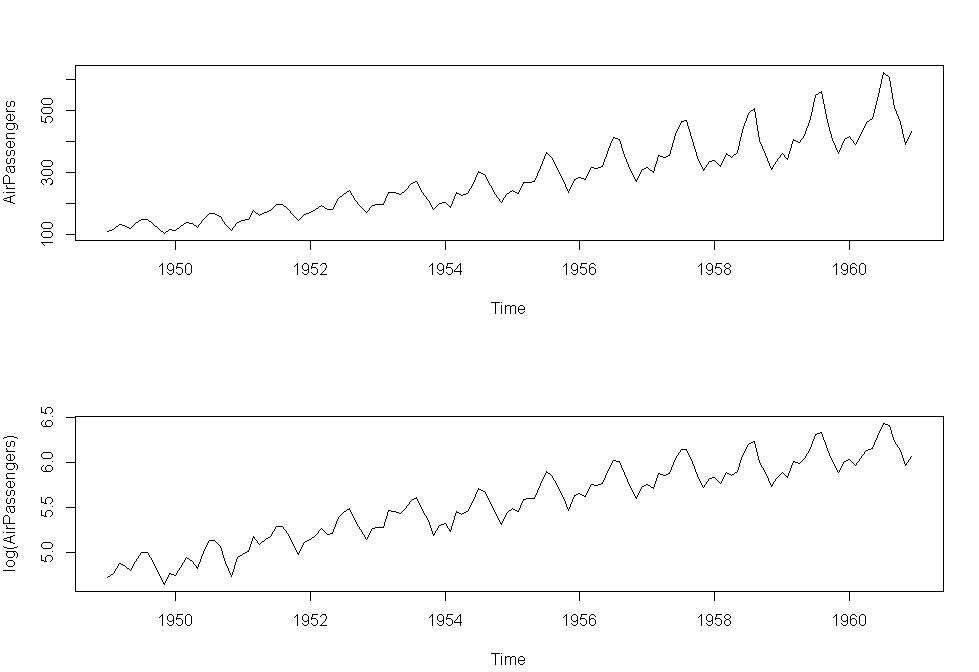

#季节性分解

plot(AirPassengers)

lAirPassengers<-log(AirPassengers)

plot(lAirPassengers,ylab="log(AirPassengers)")

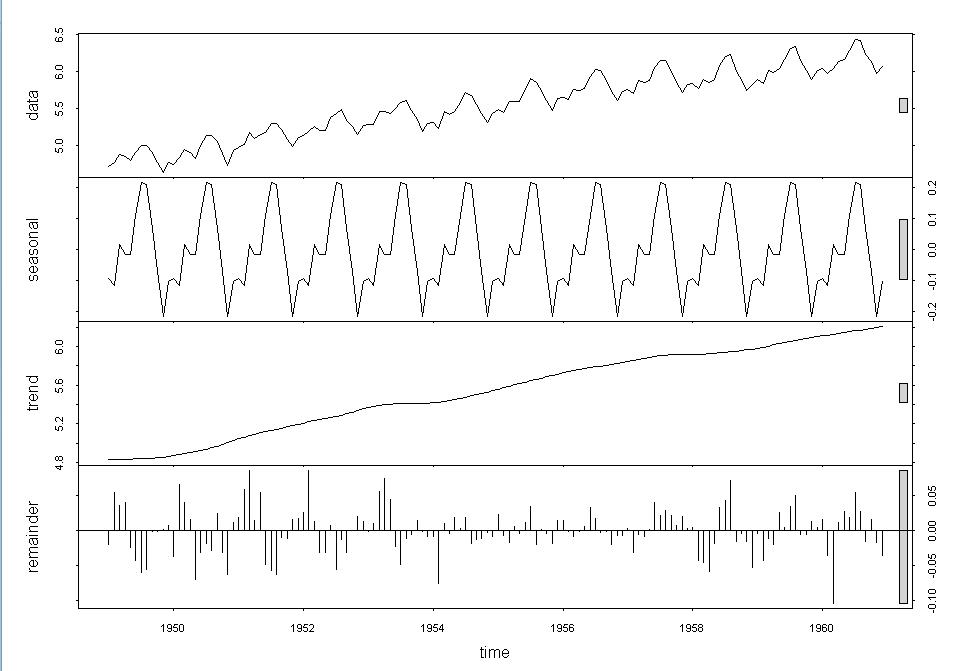

fit<-stl(lAirPassengers,s.window="period")

plot(fit)

fit$time.series

exp(fit$time.series)

par(mfrow=c(2,1))

library(forecast)

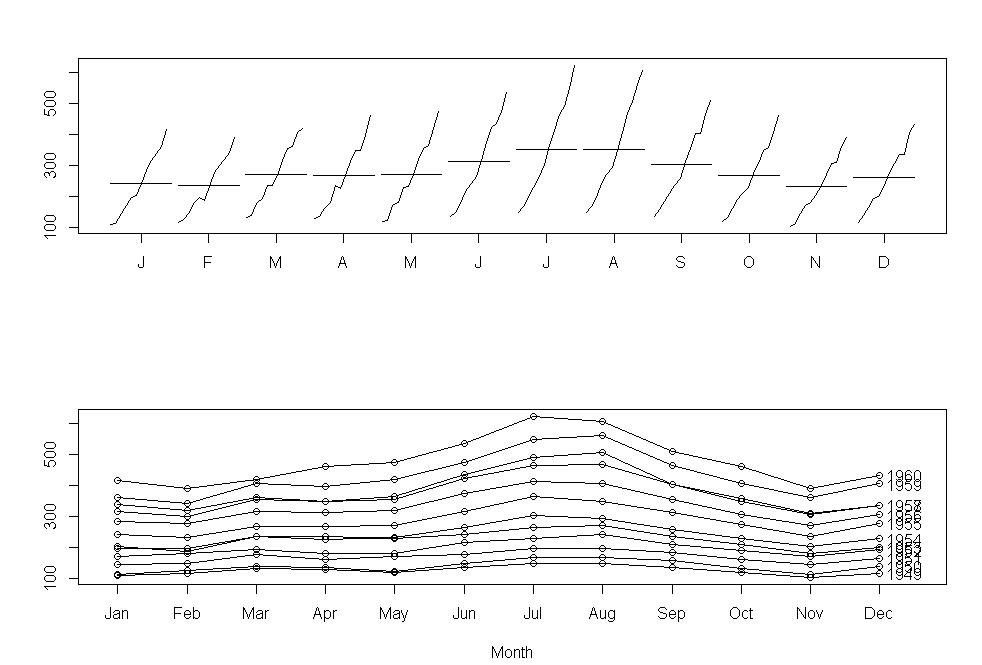

monthplot(AirPassengers,xlab="",ylab="")

seasonplot(AirPassengers,year.labels="TRUE",main="")

#单指数平滑

library(forecast)

fit<-ets(nhtemp,model="ANN")

fit

ETS(A,N,N)

Call:

ets(y = nhtemp, model = "ANN")

Smoothing parameters:

alpha = 0.182

Initial states:

l = 50.2759

sigma: 1.1263

AIC AICc BIC

265.9298 266.3584 272.2129

forecast(fit,1)

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

1972 51.87045 50.42708 53.31382 49.66301 54.0779

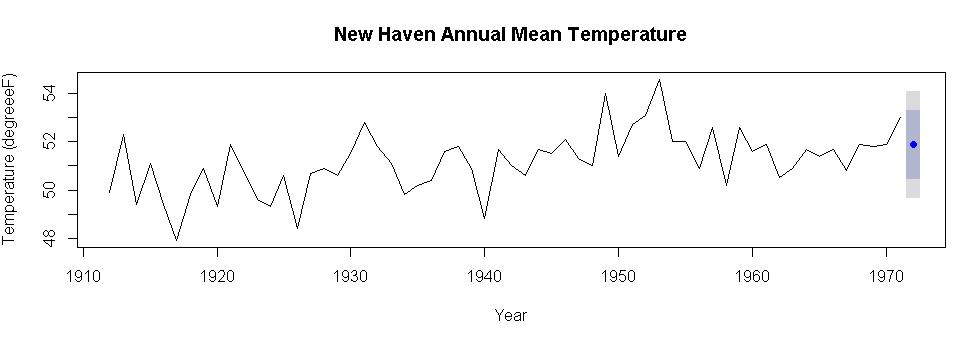

plot(forecast(fit,1),xlab="Year",ylab=expression(paste("Temperature (",degreee*F,")",)),main="New Haven Annual Mean Temperature")

accuracy(fit)

ME RMSE MAE MPE MAPE MASE ACF1

Training set 0.1460295 1.126268 0.8951331 0.2418693 1.748922 0.7512497 -0.00653111

ME: Mean Error

RMSE: Root Mean Squared Error

MAE: Mean Absolute Error

MPE: Mean Percentage Error

MAPE: Mean Absolute Percentage Error

MASE: Mean Absolute Scaled Error

ACF1: Autocorrelation of errors at lag 1.

#有水平项,斜率以及季节性的指数模型

library(forecast)

fit<-ets(log(AirPassengers),model="AAA")

fit

ETS(A,A,A)

Call:

ets(y = log(AirPassengers), model = "AAA")

Smoothing parameters:

alpha = 0.6534

beta = 1e-04

gamma = 1e-04

Initial states:

l = 4.8022

b = 0.01

s=-0.1047 -0.2186 -0.0761 0.0636 0.2083 0.217

0.1145 -0.011 -0.0111 0.0196 -0.1111 -0.0905

sigma: 0.0359

AIC AICc BIC

-208.3619 -203.5047 -157.8750

accuracy(fit)

pred<-forecast(fit,5)

pred

ME RMSE MAE MPE MAPE MASE ACF1

Training set -0.0006710596 0.03592072 0.02773886 -0.01250262 0.508256 0.2291672 0.09431354

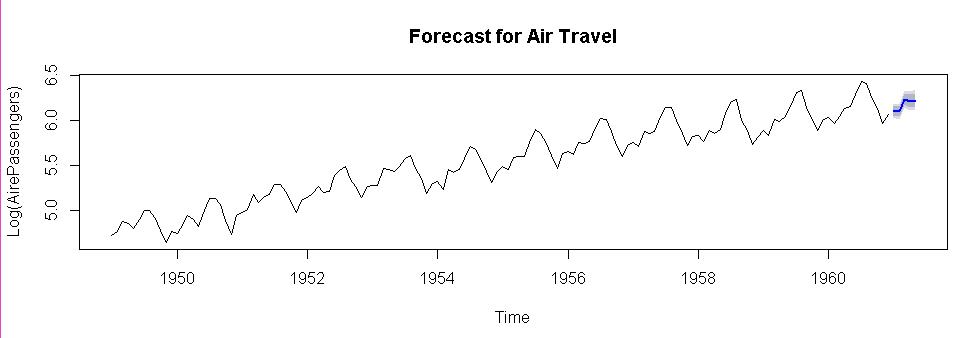

plot(pred,main="Forecast for Air Travel",ylab="Log(AirePassengers)",xlab="Time")

pred$mean<-exp(pred$mean)

pred$lower<-exp(pred$lower)

pred$upper<-exp(pred$upper)

p<-cbind(pred$mean,pred$lower,pred$upper)

dimnames(p)[[2]]<-c("mean","Lo 80","Lo 95","Hi 80","Hi 95")

p

mean Lo 80 Lo 95 Hi 80 Hi 95

Jan 1961 447.4958 427.3626 417.0741 468.5774 480.1365

Feb 1961 442.7926 419.1001 407.0756 467.8245 481.6434

Mar 1961 509.6958 478.7268 463.1019 542.6682 560.9776

Apr 1961 499.2613 465.7258 448.8949 535.2116 555.2788

May 1961 504.3514 467.5503 449.1688 544.0491 566.3135

#ETS函数的自动指数预测

library(forecast)

fit<-ets(JohnsonJohnson)

fit

ETS(M,A,M)

Call:

ets(y = JohnsonJohnson)

Smoothing parameters:

alpha = 0.1481

beta = 0.0912

gamma = 0.4908

Initial states:

l = 0.6146

b = 0.005

s=0.692 1.2644 0.9666 1.077

sigma: 0.0889

AIC AICc BIC

166.6964 169.1289 188.5738

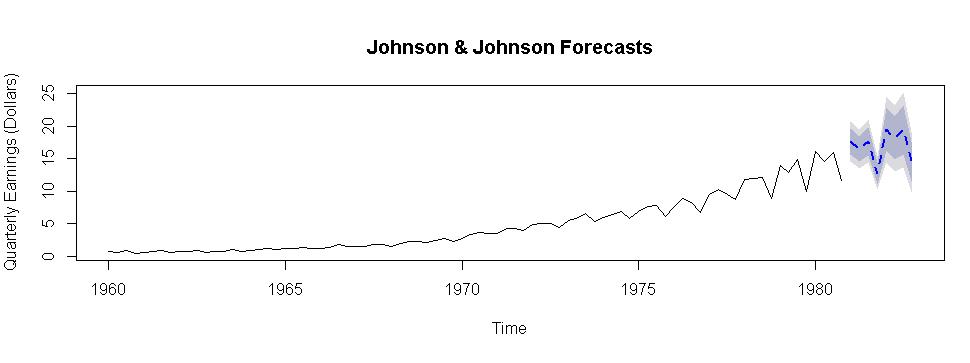

plot(forecast(fit),main="Johnson & Johnson Forecasts",ylab="Quarterly Earnings (Dollars)",xlab="Time",flty=2)

#序列的变换以及稳定性评估

library(forecast)

library(tseries)

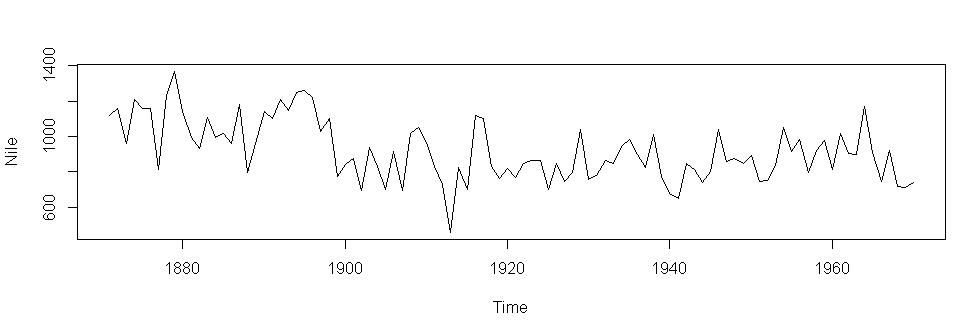

plot(Nile)

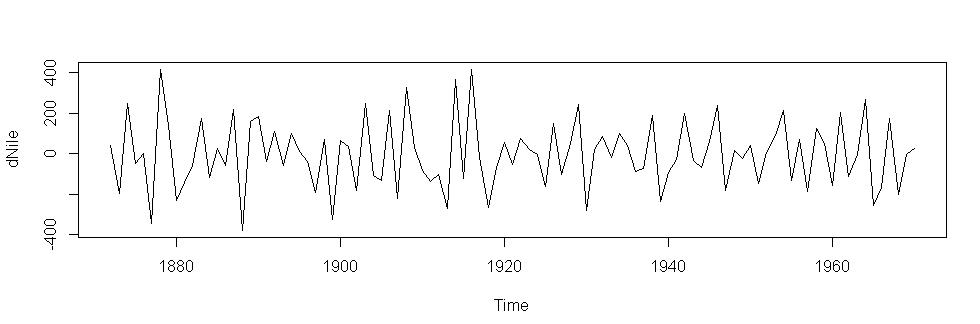

ndiffs(Nile)

[1] 1

dNile<-diff(Nile)

plot(dNile)

#拟合ARIMA模型

library(forecast)

fit<-arima(Nile,order=c(0,1,1))

fit

accuracy(fit)

ME RMSE MAE MPE MAPE MASE ACF1

Training set -11.9358 142.8071 112.1752 -3.574702 12.93594 0.841824 0.1153593

#模型评价

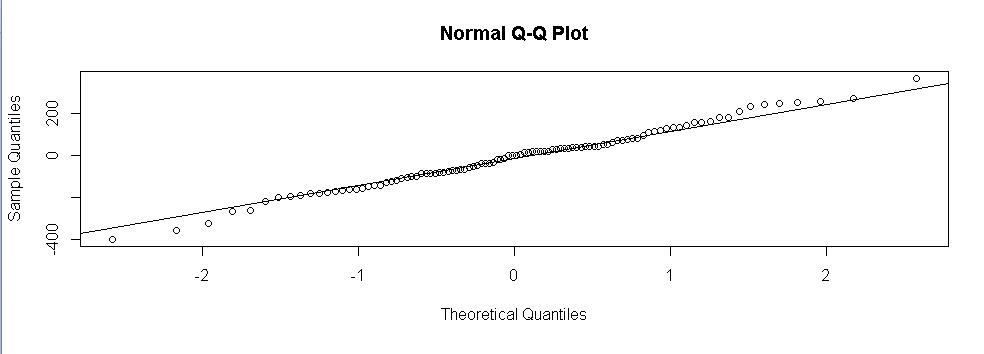

qqnorm(fit$residuals)

qqline(fit$residuals)

Box.test(fit$residuals,type="Ljung-Box")

Box-Ljung test

data: fit$residuals

X-squared = 1.3711, df = 1, p-value = 0.2416

#ARIMA 模型预测

forecast(fit,3)

plot(forecast(fit,3),xlab="Year",ylab="Annual Flow")

#ARIMA自动预测

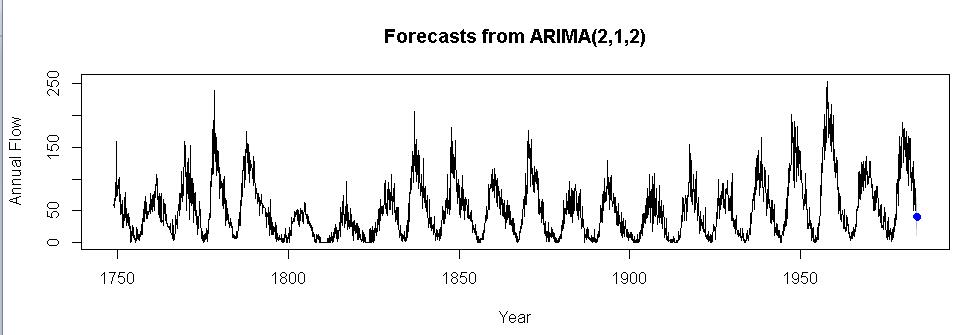

library(forecast)

fit<-auto.arima(sunspots)

fit

Series: sunspots

ARIMA(2,1,2)

Coefficients:

ar1 ar2 ma1 ma2

1.3467 -0.3963 -1.7710 0.8103

s.e. 0.0303 0.0287 0.0205 0.0194

sigma^2 estimated as 243.8: log likelihood=-11745.5

AIC=23500.99 AICc=23501.01 BIC=23530.71

forecast(fit,3)

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

Jan 1984 40.43784 20.42717 60.44850 9.834167 71.04150

Feb 1984 41.35311 18.26341 64.44281 6.040458 76.66576

Mar 1984 39.79670 15.23663 64.35677 2.235319 77.35808

accuracy(fit)

ME RMSE MAE MPE MAPE MASE ACF1

Training set -0.02672716 15.60055 11.02575 NaN Inf 0.4775401 -0.01055012

小结

这章主要讲解了怎么用R语言来进行时间序列分析,例如:模型的建立,图表的绘制,以及未来趋势的预测。这类型的数据分析完全不在程序开发的范畴了,所有的分析都是基于数理统计,这应该就是现在的数据科学方向吧。

以上是关于R语言学习笔记(十三):时间序列的主要内容,如果未能解决你的问题,请参考以下文章