期货策略:卖出涨幅较大期货合约,买入涨幅较小期货合约

Posted

tags:

篇首语:本文由小常识网(cha138.com)小编为大家整理,主要介绍了期货策略:卖出涨幅较大期货合约,买入涨幅较小期货合约相关的知识,希望对你有一定的参考价值。

策略想法:选择期货锌和期货铜2016年主力合约小时数据,如果买入 前一小时涨幅较大合约,假设A,买入前一小时涨幅较小合约,假设B,买入时实时保持两者价值相等(价格不相等,则买入份数不一样),如果A涨幅小于B涨幅,则平仓。

策略代码如下:

import pandas as pd

import pyodbc

from sqlalchemy import create_engine

import numpy as np

from statistics import median

import crash_on_ipy

import pdb

import matplotlib.pyplot as plt

from numpy import nan

data_cu=pd.read_csv(‘SQCU13.csv‘)

data_zn=pd.read_csv(‘SQZN13.csv‘)

data_zn.columns=[‘date‘,‘time‘,‘open‘,‘high‘,‘low‘,‘close‘,‘volumn‘,‘hold‘]

data_cu.columns=[‘date‘,‘time‘,‘open‘,‘high‘,‘low‘,‘close‘,‘volumn‘,‘hold‘]

data_zn[‘date_time‘]=data_zn[‘date‘]+data_zn[‘time‘]

data_cu[‘date_time‘]=data_cu[‘date‘]+data_cu[‘time‘]

del data_zn[‘date‘],data_zn[‘time‘],data_cu[‘date‘],data_cu[‘time‘]

data_zn=data_zn.set_index(‘date_time‘)

data_cu=data_cu.set_index(‘date_time‘)

data_zn.rename(index=lambda x:str(x)[:12],inplace=True)

data_cu.rename(index=lambda x:str(x)[:12],inplace=True)

#取收盘价

data_zn=data_zn.loc[:,[‘close‘]]

data_cu=data_cu.loc[:,[‘close‘]]

new_data_zn=data_zn.groupby(data_zn.index).last()

new_data_cu=data_cu.groupby(data_cu.index).last()

data=pd.concat([new_data_zn,new_data_cu],axis=1)

data.columns=[‘zn_close‘,‘cu_close‘]

data_zn_array=np.array(new_data_zn[‘close‘])

data_cu_array=np.array(new_data_cu[‘close‘])

T=len(data_zn_array)

zn_return=[0]

cu_return=[0]

mark_enter=[0]*(T)

mark_leave=[0]*(T)

for i in range(1,T):

if new_data_zn.index[i]==new_data_cu.index[i]:

zn_return.append((data_zn_array[i]-data_zn_array[i-1])/data_zn_array[i])

cu_return.append((data_cu_array[i]-data_cu_array[i-1])/data_cu_array[i])

data[‘zn_return‘]=zn_return;data[‘cu_return‘]=cu_return

profit=[]

position=False

long_zn_positon=False

for i in range(1,T):

if data[‘zn_return‘][i]<data[‘cu_return‘][i] and not position:

position=True

long_zn_positon=True

mark_enter[i]=1

shares=data[‘cu_close‘][i]/data[‘zn_close‘][i]

long_price=data[‘zn_close‘][i]

short_price=data[‘cu_close‘][i]

elif data[‘zn_return‘][i]>data[‘cu_return‘][i] and not position:

position=True

long_zn_positon=False

shares = data[‘cu_close‘][i]/ data[‘zn_close‘][i]

mark_enter[i]=1

long_price = data[‘cu_close‘][i]

short_price = data[‘zn_close‘][i]

elif data[‘zn_return‘][i]>data[‘cu_return‘][i] and position and long_zn_positon:

position=False

long_zn_positon = False

mark_leave[i]=1

return_zn=(data[‘zn_close‘][i]-long_price)*shares

return_cu=short_price-data[‘cu_close‘][i]

profit.append((return_zn+return_cu)/(2*short_price))

elif data[‘zn_return‘][i]<data[‘cu_return‘][i] and position and not long_zn_positon:

position=False

long_zn_positon=False

mark_leave[i]=1

return_zn=(short_price-data[‘zn_close‘][i])*shares

return_cu=long_price-data[‘cu_close‘][i]

profit.append((return_zn + return_cu) / (2 * long_price))

#计算sharpe

#计算总回报

total_return=np.expm1(np.log1p(profit).sum())

#计算年化回报

annual_return=(1+total_return)**(365/365)-1

risk_free_rate=0.015

profit_std=np.array(profit).std()

volatility=profit_std*(len(profit)**0.5)

annual_factor=1

annual_volatility=volatility*((annual_factor)**0.5)

sharpe=(annual_return-risk_free_rate)/annual_volatility

# print(total_return,annual_return,std,volatility,annual_volatility,sharpe)

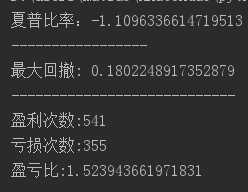

print(‘夏普比率:{}‘.format(sharpe))

#计算最大回撤

#计算

df_cum=np.exp(np.log1p(profit).cumsum())

max_return=np.maximum.accumulate(df_cum)

max_drawdown=((max_return-df_cum)/max_return).max()

print(‘-----------------‘)

print(‘最大回撤: {}‘.format(max_drawdown))

#计算盈亏比plr

win_times=sum(x>0 for x in profit)

loss_times=sum(x<0 for x in profit)

plr=win_times/loss_times

print(‘----------------------------‘)

print(‘盈利次数:{}‘.format(win_times))

print(‘亏损次数:{}‘.format(loss_times))

print(‘盈亏比:{}‘.format(plr))

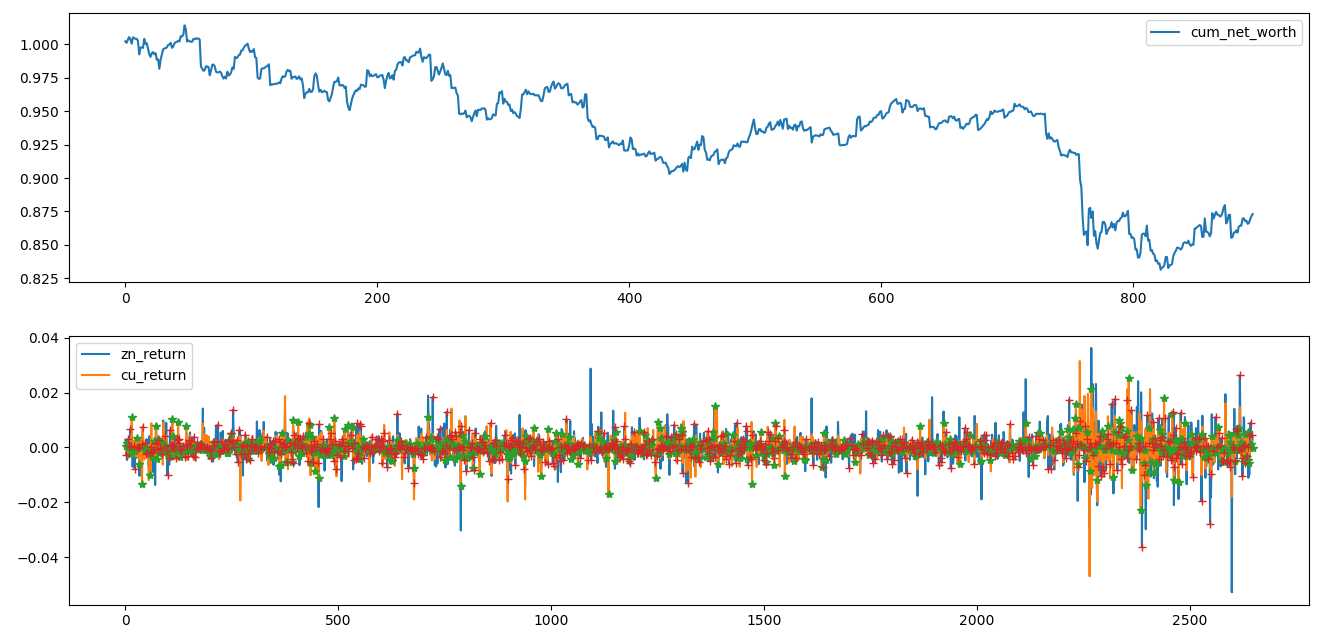

# #画出净值走势图

fig=plt.figure()

ax1=fig.add_subplot(2,1,1)

cum_net_worth,=plt.plot(df_cum,label=‘cum_net_worth‘)

plt.legend([cum_net_worth],[‘cum_net_worth‘])

ax2=fig.add_subplot(2,1,2)

zn,=plt.plot(zn_return)

cu,=plt.plot(cu_return)

plt.legend([zn,cu],[‘zn_return‘,‘cu_return‘])

for i in range(0,T):

if mark_enter[i]==0:

cu_return[i]=nan

plt.plot(cu_return,‘*‘)

for i in range(0,T):

if mark_leave[i]==0:

zn_return[i]=nan

plt.plot(zn_return,‘+‘)

plt.show()

pdb.set_trace()

策略运行结果如下图:

以上是关于期货策略:卖出涨幅较大期货合约,买入涨幅较小期货合约的主要内容,如果未能解决你的问题,请参考以下文章