寻找一篇关于企业年金的英文资料

Posted

tags:

篇首语:本文由小常识网(cha138.com)小编为大家整理,主要介绍了寻找一篇关于企业年金的英文资料相关的知识,希望对你有一定的参考价值。

最好是关于政府在企业年金建设中的责任和作用方面的,实在不行,只要和企业年金有关就行... 大家帮忙... 谢谢.. 急..

最好是论文形式的,谢谢大家了,回答后还有加分

The past few years have witnessed some major changes to the UK pensions landscape. New legislation introduced in April 2006 (A-day) has had particular implications for the insurance-administered occupational pensions sector, removing many of the distinctions between trust-based and contract-based schemes - thus enhancing the attractiveness of the latter to employers.

Yet more change is on the horizon, in the form of personal accounts. While the idea of introducing a national pension savings scheme is viewed as a step in the right direction by pension providers and advisers, there are concerns over how the scheme can be effectively administered within proposed cost limitations and what will be the impact on existing arrangements.

Table of Contents

Issues in the Market

Key issues

Market definitions

Figure 1: Types of private pension provision, UK

Occupational schemes

Defined-benefit (salary-related) schemes

Defined-contribution (money-purchase) schemes

Other work-related pensions

Other definitions

Abbreviations

Market in Brief

Active membership continues to recede

Scheme administration and funding

New insurance-administered business up strongly in 2006

Improvements in the equity and bond markets help to reduce deficits

Regulatory changes boost appeal of outsourcing

Product developments centre on risk-sharing solutions

FTSE 100 firms run the largest private-sector schemes

Top five players in the insurance-administered sector control three fifths of the market

IFAs generate the lion' s share of insurance-administered sales

Minimal above-the-line advertising

An occupational scheme is the most common pension type

Figure 2: Proportion of adults who are active members of a pension, by type, April 2007

Occupational DC scheme members have shorter investment terms

Figure 3: Number of years making pension contributions, by type of pension, April 2007

Merely half of those with the freedom to switch funds actually do so

Figure 4: Attitudes and experiences of occupational pension scheme members, April 2007

Promising public support for personal accounts

Broader Market Environment

Key points

Greater inducement for people to save

Figure 5: Total PDI, consumer expenditure and savings, 2003-12

Implication

Steady economic growth

Figure 6: GDP annual growth and proportion of workforce unemployed -- UK, 1997-2007

Higher inflation requires pension savings to work harder

Figure 7: Average annual changes in the bank base rate, CPI and RPI -- UK, 1997-2007

Implication

Asset allocation weighted towards equities

Rising stock markets help to reduce pension fund deficits

Figure 8: FTSE 100 and FTSE All Share -- daily index movements, May 1997-May 2007

Implication

What does this mean for the future of DB schemes?

Could some schemes reopen?

Corporate UK needs to wake up to the longevity risk

Figure 9: Cohort life expectancy at age 60, by gender, 1981-2054

Implication

Recommendation

An ageing population puts greater stress on pension funds

Figure 10: Projected size of the UK population, by age band, 2007-44

Implication

New age discrimination laws means more workers will retire later

Internal Market Environment

Key points

A pension forms an integral part of the benefits package

Figure 11: Top five company benefits and top five most desired, January 2007

Most common type is still a final-salary pension

Routes to closure

PPF levy is an extra cost burden

Reducing pension liabilities

The Money-purchase movement

Transfer of risk

Contribution rates are much lower for DC schemes

Figure 12: Employer and employee contribution rates for active members of private-sector occupational pension schemes, by type of scheme, 2004 and 2005

Apathy reigns

Few employees keep track of their fund' s performance

Implication and recommendation

A minority of workers shun or defer joining the company scheme

Implication and recommendation

Pensions simplification

Admin upheaval for trustees and administrators

New opportunities for life and pensions companies

Further reform

The Pensions Regulator exerts its influence

Trigger points

Improving trustee knowledge

Competitive Context

Pension substitutes

Figure 13: Summary of retirement funding strategies

Growing number of amateur property investors

The pension-ISA combo

Equity release provides a solution for some

Strengths and Weaknesses in the Market

Figure 14: Occupational/group pensions -- SWOT analysis, 2007

Scheme Size and Membership

Key points

Private-sector schemes in decline

Figure 15: Number of private-sector occupational pension schemes in the UK, by scheme size, 2002-06

Implication

Just 6% of private-sector employers run an occupational scheme

Only half the number of private-sector schemes were open in 2006

Figure 16: Status of private-sector schemes, 2006

DC schemes make up the majority of occupational pensions

Figure 17: Number of private-sector occupational schemes, by benefit structure and size band, 2005

Active membership has also declined over the past decade

Figure 18: Number of private-sector occupational scheme members, 1995-2006

Note on double counting

Three in four members were contracted out in 2006

Figure 19: Active members of private-sector schemes, by route to being contracted-out, 2006

One in ten active members were paying AVCs in 2005

Public-service sector

Value of Funded Pensions

Key points

Framework for workplace pensions

Figure 20: Types of workplace pension, 2007

Outsource or in-house?

The self-administered sector is the largest in value

Figure 21: Value of assets in funded pensions, 1997-2005

Implication

A note about the data

Pension Contributions

Key points

Employers up their contributions to reduce deficits

Figure 22: Contributions to private pension schemes -- UK, 2001-05

Insurance-Administered Sector

Key points

In-force business continues to decline

Figure 23: Insurance-administered occupational pension business in force, 2001-05

Lump-sum investment drives new business growth...

Figure 24: New insurance-administered occupational pension business, 2001-06

...mainly in the area of TIPs and buyouts

Figure 25: New insurance-administered occupational pension business, by sub-sector, 2005 and 2006

Providers take the long view to the buyout market

Single-premium business will continue to grow strongly

Figure 26: Forecast of new insurance-administered occupational business, 2006-11

In-force GPP business

Figure 27: GPP business in force, 2001-05

New GPP sales soar

Figure 28: New GPP business, 2001-06

Implication

New GPP business set to rocket

Figure 29: Forecast of new GPP business, 2006-11

Factors incorporated

Market Share

Key points

Prudential tops the rankings in the insurance-administered sector

Figure 30: Top 20 insurance companies in the occupational pensions market, by net premiums, 2004 and 2005

Individual pensions sector

The largest plcs are among the largest employers in the UK

Figure 31: The top 20 listed companies by market capitalisation, January 2007

Companies and Products

Supply structure

Figure 32: The main participants in the occupational pensions market

Employers

Insurance companies

Prudential

Legal & General

Standard Life

Investment management

Pensions IFAs

Benefit consultants

Other professional services

Brand Communication and Promotion

Key points

Pensions adspend dips following A-Day

Figure 33: Total advertising expenditure on pension and annuity products, 2005-07

Limited use of consumer advertising...

...but investment is likely to rise over the coming years

Hargreaves Lansdown tops the pensions advertiser rankings

Figure 34: Advertising expenditure by the top ten pensions advertisers, 2006 and 2007

Channels to Market

Key points

Most group pension business is sold with advice

Non-intermediated channel represents a small but growing share of new regular-premium group pensions business

Figure 35: Distribution breakdown of new insurance -- administered occupational pension business -- regular premium, 2001-06

IFAs win the lion' s share of single-premium group pensions business

Figure 36: Distribution breakdown of new insurance -- administered occupational pension business -- single premium, 2001-06

Implication

The Consumer -- Pension Participation

Key points

Survey background

Less than a third of non-retired adults are members of an occupational pension

Figure 41: Proportion of adults who are active members of a pension, by type, April 2007

Paid-up pensions

Transfers made easier

One in ten occupational scheme members are saving in a personal pension

Figure 42: Cross-analysis of pension types, April 2007

Small decline in those contributing to DB schemes

Figure 43: Proportion of adults who are active members of a pension, by type, 2006 and 2007

Implication

Shift in the direction of SIPPs

Implication

Still much confusion over pension type

Figure 44: Proportional split of occupational schemes, by benefit type, 2006 and 2007

Implication

Gender gap is much narrower in the occupational pension sector

Figure 45: Proportion of adults who are active members of a pension, by type and by gender, age, socio-economic group, marital status, lifestage and Special Group, April 2007

Implication

Pension participation peaks in the 45-54 age group

Implication

Ownership levels are highest among the wealthier groups

Figure 46: Proportion of adults who are active members of a pension, by type and by tenure, working status, gross annual household income, ACORN category and region, April 2007

Implication

Raise awareness and build the brand via broadsheet ads

Figure 47: Proportion of adults who are regularly contributing to a pension, by type and by new technology usage, newspaper readership, commercial TV viewing and supermarket usage, April 2007

Implication and opportunity

CHAID analysis

Figure 48: Target groups identified for the occupational and personal pensions markets, April 2007

Driver 1: employment

Driver 2: income

Driver 3: age

Implication and opportunity

The Consumer -- Length of Contributions

Key points

DB scheme members have been saving for longer than their DC counterparts

Figure 49: Number of years making pension contributions, by type of pension, April 2007

Implication

Sharp fall in the proportion of new joiners to occupational schemes

Figure 50: Number of years making occupational pension contributions, 2006 and 2007

Implication

A small proportion of adults have left starting a pension late

Figure 51: Number of years making pension contributions, by gender, age and socio-economic group, April 2007

Implication

The Consumer -- Attitudes and Experiences

Key points

Around half of occupational scheme members were auto-enrolled

Figure 52: Attitudes and experiences of group pension scheme members, April 2007

Implication

DB schemes have greater pulling power

Implication: employer contributions are essential

One in eight members have the option to the select their own funds

Implication

Inform and educate to engage members

Figure 53: Cross-analysis of attitudes and experiences of group pension scheme members, April 2007

Implication

C2DEs are less enthused about their pension

Figure 54: Attitudes and experiences of group pension scheme members, by gender and socio-economic group, April 2007

Younger members particularly need better access to info and advice

Figure 55: Attitudes and experiences of group pension scheme members, by age group, April 2007

Implication

Recent joiners are more likely to have a choice of funds

Figure 56: Attitudes and experiences of group pension scheme members, by length of time making contributions, April 2007

参考资料:http://www.giichinese.com.cn/chinese/mt53789-uk-pensions.html

指数基金介绍专栏:国企指数(H股指数)详细介绍,最新资料解析,看这一篇就够了

作者:牛大 | 公众号:定投五分钟

大家好,我是牛大。每天五分钟,投资你自己;坚持基金定投,终会财富自由!

昨天牛大给大家介绍了恒生指数,没看的朋友可以去公众号看一下。

指数基金介绍专栏(7):恒生指数

对于H股指数,估计大部分朋友不是特别了解。牛大也查了一些最新的资料,尽力给大家介绍一下,希望大家能多了解一些。

恒生中国企业指数(简称:国企指数或H股指数),为投资者提供一个反映在香港上市的中国企业的股价表现的指标。

有时简称为国企指数的时候,有朋友会误认为是中国的所有国有企业组成的指数。

其实这里的国企指的是在香港上市的中国企业,虽然在香港上市的大部分公司为国有企业。此国企非彼国企,大家应该明白了吧。

与恒生指数不同的是,国企指数成份股的数目并没有限制,但必须为市值最大,且在恒生综合指数成份股内的H股。国企指数也是由恒生银行属下恒生指数有限公司负责计算。

国企指数于1994年8月8日首次公布,以上市H股公司数目达到10家的日期,即1994年7月8日为基数日。当日收市指数定为1000点,该指数以所有在香港联交所上市的中国H股公司股票为成份股计算得出加权平均股价指数。

咱们选择的H股指数基金为易方达恒生国企ETF联接A(110031),是一款2012年成立的老牌基金。

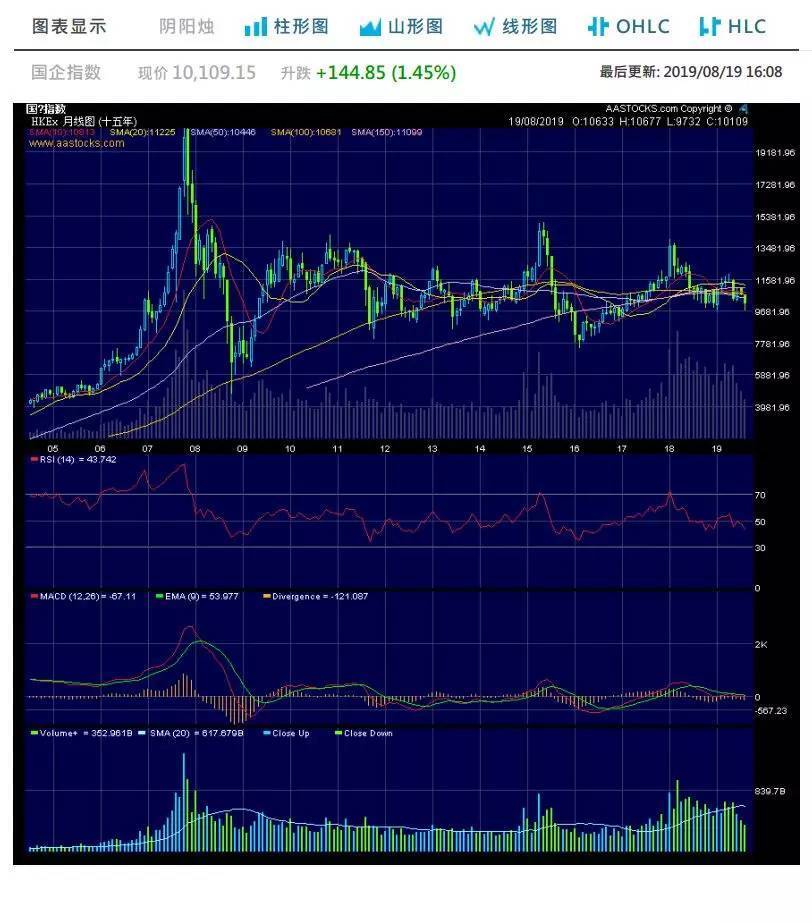

目前(2019年8月19日)H股指数点位为10109.15点,1994年起始为1000点,总共涨了10倍多。历史最高为2007年11月1日,恒生中国企业指数曾突破20600点,最高见20609.10点。算上这二十多年的分红,有将近20-30倍的收益。收益也是非常的不错。

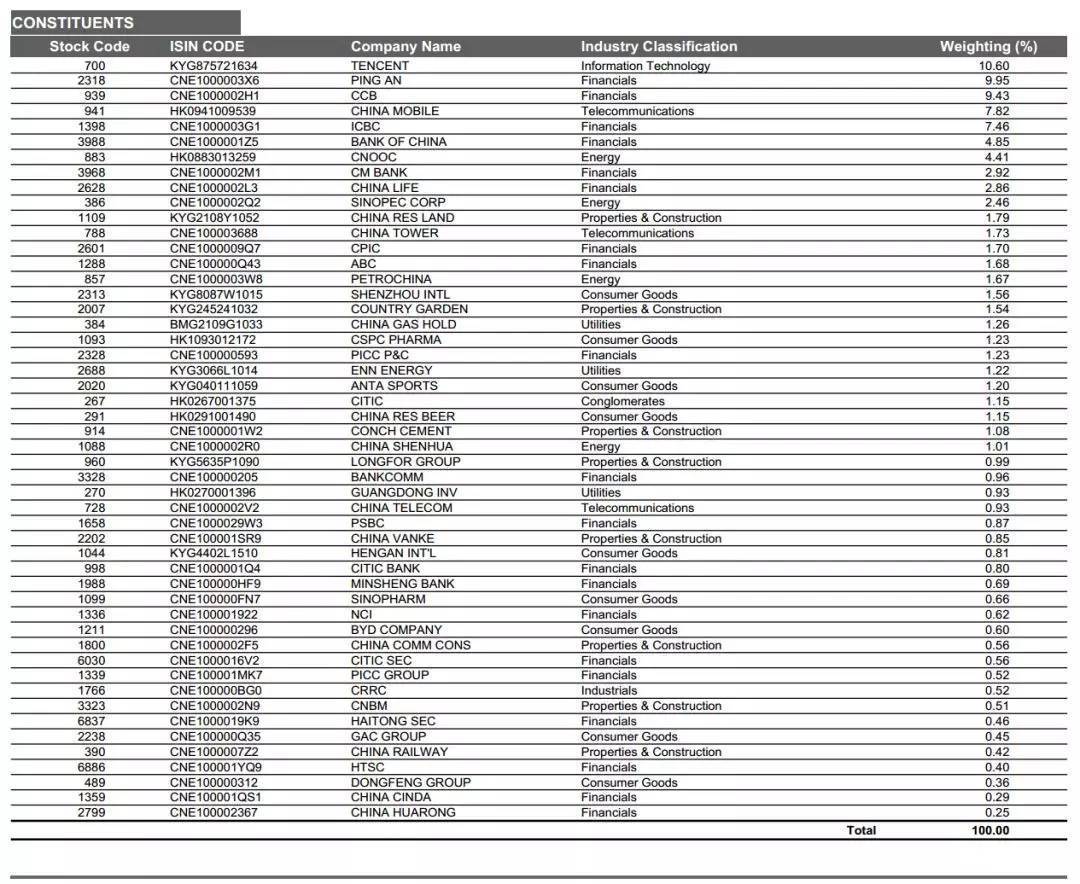

截止到目前(2019年8月19日)为止,H股指数的成分股数量已经扩容到了50只,如下图所示。占权重第一位的大家也许没想到,是一家私有企业,大家基本每天都在用它的产品。各位朋友们不用猜了,它就是腾讯,权重占比10.6%。

牛大给大家翻译一下,排名前十的分别是:腾讯,中国平安,中国建设银行,中国移动,中国工商银行,中国银行,中海油,招商银行,中国人寿,中国石油化工。前十名权重占比总共为:62.76%。感兴趣的朋友可以通过英文名称查一下其它公司是何方神圣。

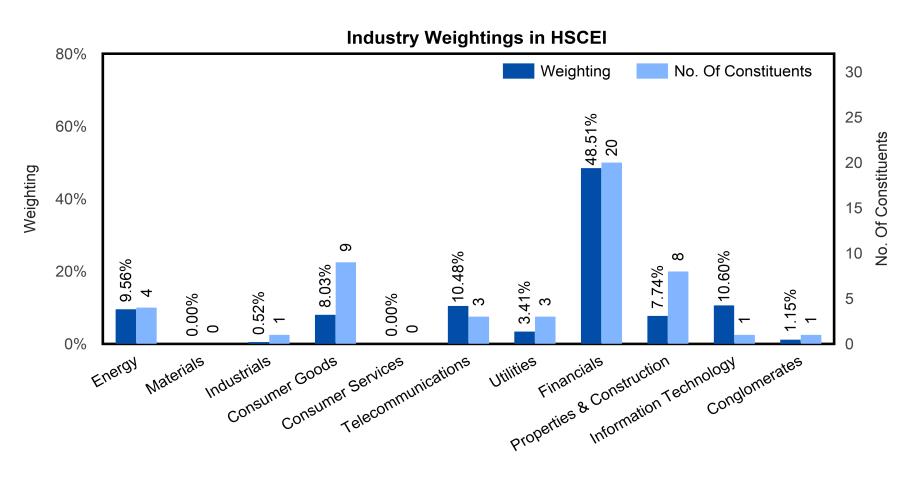

从上图可以看出,按行业来分,权重占比最高的是金融行业,共有20家公司,占比48.51%。次之的分别为为信息技术与通信行业。

等H股指数性价比很高的时候,牛大会带领大家一起定投H股指数,帮助咱们盈利锦上添花。好了,今天牛大就给大家介绍到这里,祝大家生活愉快!

每天花5分钟收看牛大的文章,一起定投基金赚钱。剩下的苦活累活就都交给牛大吧,这也是我每天努力在为大家做的。

每天五分钟,投资你自己。相信牛大:一起努力,咱们终将富有!

以上是关于寻找一篇关于企业年金的英文资料的主要内容,如果未能解决你的问题,请参考以下文章